In the final piece of our Small Business Week series, we'll talk about tracking transactions via blockchain and if your business should use this technology.

Small Business Week is almost over, and today we're talking about a technology that has changed the way businesses everywhere see money and transactions: blockchain.

Do you need be one of the companies using blockchain technology? Let's find out.

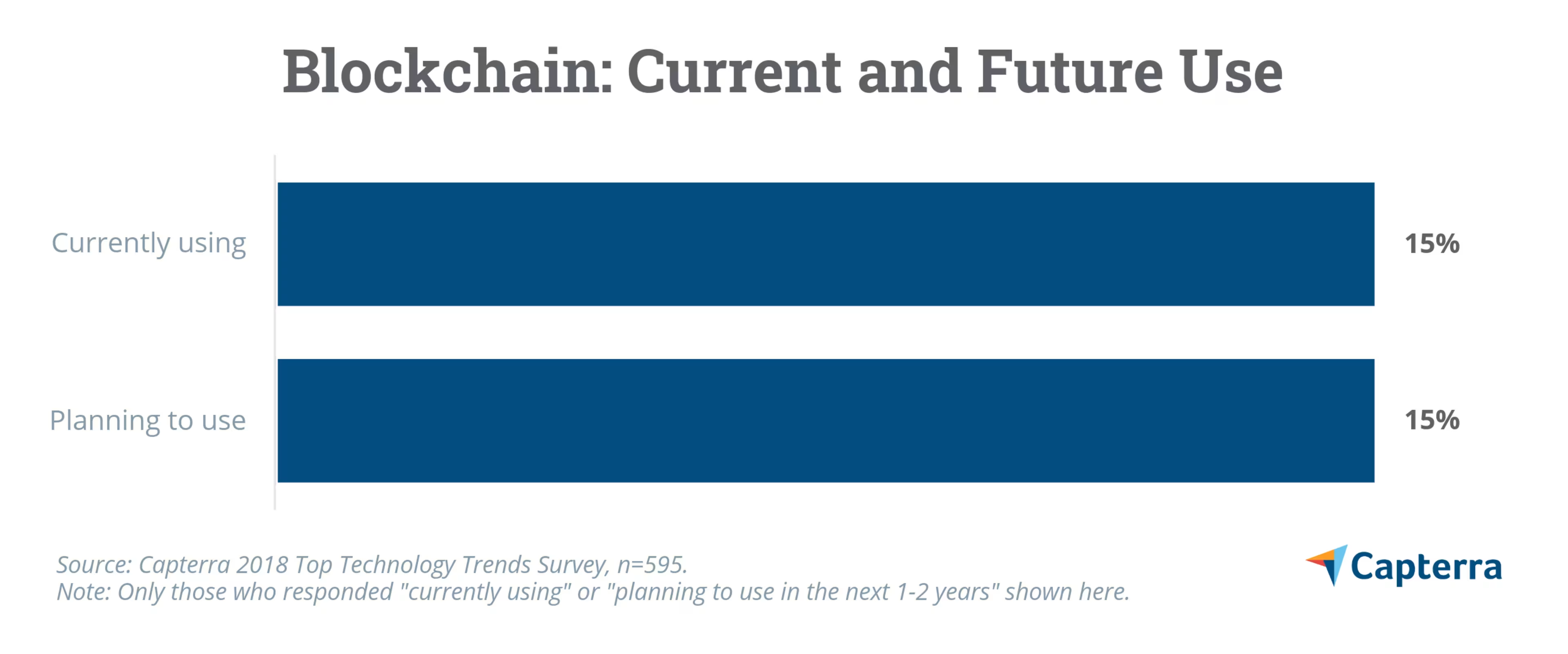

Over 15% of the small and midsize businesses (SMBs) we surveyed are currently using blockchain. Another 15% intend to use blockchain in the next 12 to 24 months.

At its core, blockchain allows for a secure, decentralized way of record-keeping for transactions. Still trying to wrap your head around the concept of blockchain? Read this first.

Blockchain has been adopted by a large part of the finance and accounting industries, and the healthcare and legal industries are moving in that direction as well.

Do you need blockchain for your bakery? No.

Do you need blockchain for your accounting firm or medical practice? Possibly, depending on the number of transactions and records you're trying to timestamp. Read on for more discussion of blockchain.

Companies using blockchain technology in real life

Eric Brown from Aliant Payments says, “After 16 years of offering traditional payment solutions (mainly credit and debit card), we realized that blockchain was at the forefront of our industry, so we embraced it and saw it as a way to innovate and stay ahead of our competitors."

The banking and finance sectors have been the primary adopters of blockchain with the invention of Bitcoin, although blockchain was developed in the early '90s.

Our clients look to us for ways to transfer money safely, securely, and cost-effectively, and cryptocurrency allows us to move money in all of these ways, Brown says.

It makes sense that adopting cutting-edge payment options are a big motivating factor for finance and accounting businesses because their primary focus is on the movement of money.

We designed and developed our own proprietary technology in-house, and designed it specifically for our clients. To give us even more of a competitive edge, we recently began offering our cryptoprocessing solution to qualifying merchants free of charge (something else that none of our competition is doing). This allows merchants to test out the product, and experience the benefits of cryptopayments for their business.

Adopting cryptocurrency processing, and therefore blockchain, benefits businesses that need iron-clad record keeping for transactions in bulk and that have a user base that is already trading with crypto.

Should you use it?

Blockchain and cryptocurrency are not the same thing. You can use blockchain without cryptocurrency, but you cannot use cryptocurrency without blockchain. Do you need either of these technologies at your business?

To determine if blockchain is right for your business, answer these questions:

Are you in an industry where cryptocurrency payments are becoming more mainstream?

Do your users want to be able to track the supply chain of your product—i.e., health and ethics labels such as "organic," "local," or "fair trade?"

Do you need decentralized record keeping, such as with smart contracts or health records?

Blockchain and cryptocurrency can provide transparency and security for your clients and may become a more valuable technology in sectors outside of finance as understanding and acceptance of the technology rises.

Want to learn more about blockchain?

Take a look at our articles that break down blockchain for different industries: